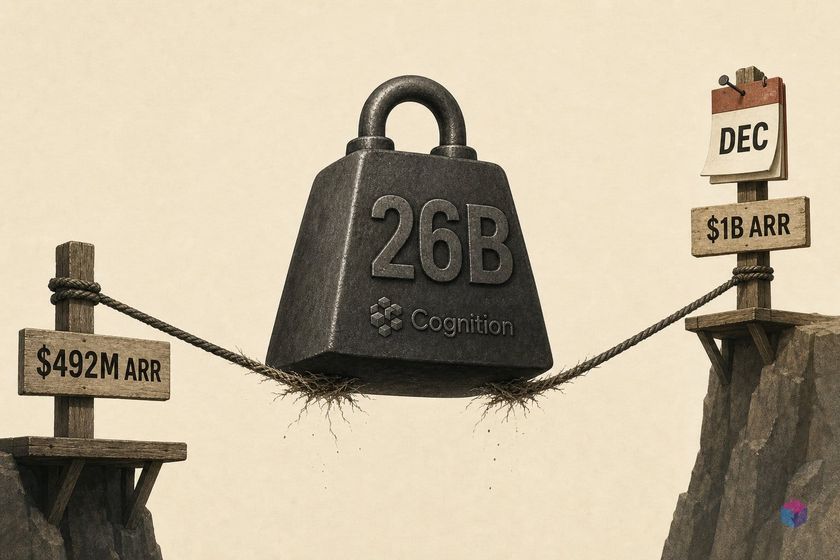

53× ARR and $26B: How to Read This Valuation

Cognition closed a Series D of more than $1 billion on May 27, 2026 at a $26 billion post-money valuation — a 53× multiple on $492 million in annualized revenue at close . That multiple is aggressive by any standard but not unprecedented for a company reporting 13× year-over-year revenue growth at this stage. The prior round — a $400 million Series C in September 2025 — valued the company at $10.2 billion post-money , making the new figure a roughly 2.5× step-up in approximately eight months. Investors are pricing in sustained hypergrowth through at least end of 2026 — specifically, Cognition needs to reach $1 billion in ARR by December to keep that multiple from looking stretched relative to current public-market comps.

Quick Answer: Cognition raised $1B+ at a $26B post-money valuation on May 27, 2026 — a 53× multiple on $492M ARR. Hitting $1B ARR before year-end 2026 requires roughly 2× growth in seven months. Thirteen-month ARR growth is reported at 13×, though figures include revenue from the Windsurf asset acquisition; organic Devin growth has not been broken out separately.

The round was co-led by Lux Capital, General Catalyst, and 8VC, with new entrants Ribbit Capital, Atreides Management, and Layer Global joining nine returning backers — including Founders Fund, Elad Gil, Soma Capital, Alpha Wave, Bain Capital Ventures, Vitruvian, Definition Capital, Conversion Capital, and 137 Ventures . The coalition is broad: generalist venture, growth equity, and fintech-focused funds across multiple risk profiles. Inclusion of Ribbit Capital — primarily known for fintech — alongside Lux and General Catalyst signals that enterprise traction in financial services is part of the underwriting. Cognition has now raised more than $2.5 billion in total since its founding in November 2023 , across four rounds in under 30 months — a capital accumulation pace that reflects both investor conviction and the infrastructure spend required to run autonomous coding agents at enterprise scale.

To calibrate the 53× multiple: it is not appropriate to compare this to mature SaaS, where 10–15× forward revenue is a ceiling. The relevant comparables are growth-stage AI application companies where year-over-year revenue velocity is the primary underwriting variable. The risk, covered in detail in the final section, is what happens when growth rate converges toward base rates and multiple compression begins. At $492M ARR and a target of $1B by December, Cognition has roughly seven months of execution data that will either validate or pressure the current mark.

| Round | Date | Size | Post-Money Valuation | Lead Investors |

|---|---|---|---|---|

| Founding / Seed | Nov 2023 | Part of $2.5B+ total | Not publicly disclosed | Founders Fund, others |

| Early rounds (combined) | 2024–early 2025 | ~$1.1B est. (residual from total) | Not publicly disclosed | Not publicly disclosed |

| Series C | Sep 2025 | $400M | $10.2B | Returning backers (not disclosed) |

| Series D | May 27, 2026 | $1B+ | $26B post-money ($25B pre-money) | Lux Capital, General Catalyst, 8VC |

From $37M to $492M: Thirteen Months of ARR Growth

Cognition's ARR reached $492 million in May 2026, up from $37 million in May 2025 — a 13× increase over twelve months . The stated target is to cross $1 billion ARR before the end of 2026, which requires roughly 2× growth from the announcement date across approximately seven months. That ask is tighter than the prior twelve-month run rate implies: the absolute net-new ARR needed ($508M+) exceeds the entire ARR base from twelve months ago, meaning the company must add more in seven months than it had total a year ago.

"More than 90% of Cognition's codebase is now written by Devin." — Scott Wu, CEO at Cognition (source: The Next Web)

Enterprise adoption reportedly grew at 50% month-over-month for six consecutive months heading into the announcement , with overall enterprise usage up more than 10× in 2026 alone. These are self-reported figures — no audited financials or independent third-party verification has been published. The company's use of its own codebase as the primary reference customer (Wu cites 89–90% of internal code written by Devin ) is credible as a product capability signal but does not substitute for third-party revenue verification.

The $1B ARR by December path maps out as follows: starting from $492M in May, the company needs to add approximately $42–45M in net new ARR per month through year-end to clear the target. At 50% MoM growth on the current base, that is arithmetically reachable. But 50% MoM on a $500M+ ARR base is a substantially harder operational lift than 50% MoM at $100M or $200M. Enterprise churn, contract renegotiations, and longer sales cycles all compound as deal sizes grow. The $1B target is achievable — it is not a foregone conclusion.

Windsurf's Assets in the Mix: Revenue, Users, and an Attribution Caveat

In July 2025, Cognition acquired the remaining assets of Windsurf — an AI coding assistant whose engineering team had been separately acquired by Google for approximately $2.4 billion earlier that year . Cognition gained Windsurf's SWE-1.6 model, hundreds of thousands of daily active users, and existing enterprise customer contracts. Google got the engineers; Cognition got the product and the revenue base. The structure of that deal — product and revenue without the talent — is notable: it is an ARR-accelerating asset purchase rather than an acqui-hire.

This creates a material information gap in reading the 13× ARR headline. The $37M figure is from May 2025 — two months before the Windsurf acquisition closed. The $492M figure is from May 2026, after Windsurf revenue and users were absorbed into Cognition's base. Cognition has not publicly broken out what portion of current ARR derives from legacy Windsurf customer contracts versus organic Devin adoption . Without that split, the growth trajectory cannot be cleanly characterized as purely product-led.

This is not a disqualifying red flag — acquisitions that accelerate ARR are standard practice, and Windsurf's enterprise customer base was real and contracted. But it is relevant for interpreting the valuation multiple. A 53× multiple priced as if on purely organic product growth is a different underwriting bet than 53× on a blended organic-plus-acquired revenue base where the organic component's trajectory is undisclosed. Institutional investors who re-upped for this round had access to internal breakdowns not available publicly; the gap matters most for external analysis and for developers or technical founders trying to assess the company's actual product-market fit trajectory.

Autonomy vs. Inline Copilot: Diverging Valuations

Cursor is Cognition's closest peer on valuation: it closed a $2.3 billion Series D at a $29.3 billion post-money valuation in November 2025 and was reportedly seeking an additional $2 billion at a $50 billion valuation as of early 2026 . At $26B, Cognition sits slightly below Cursor's November 2025 mark. Both companies are valued at levels that would have been implausible for developer tools companies in any prior funding cycle. But the architectural difference between the two products is real and drives distinct buyer profiles, pricing models, and competitive dynamics.

Cursor is an IDE-integrated assistant: it augments a developer's work inside VS Code, suggests completions, rewrites selected blocks, and runs inline. The developer approves or rejects every suggestion — the human controls the loop. Devin operates differently: given a task description, it independently plans, writes, debugs, and deploys code with no human decision required at each step . That distinction drives different pricing models — per-seat subscription for IDE tools versus task-based or outcome-based pricing for autonomous agents — and different buyers: an individual developer buys Cursor; engineering leadership or IT procurement buys Devin at contract scale.

"The infrastructure for autonomous software development represents a distinct commercial layer — not simply a feature of a foundation model, but a workflow-level product that enterprises contract separately." — from investor and analyst commentary cited in TechTimes coverage of the Series D rationale.

The model providers complicate the comparison further. Anthropic (Claude Code), OpenAI (Codex), and Google (Jules) have all launched competing autonomous coding capabilities through 2025–2026 . Unlike Cursor or Cognition, their coding tools are not separately valued — they are bundled into API pricing and subscription tiers. This makes direct valuation comparison impossible, but the structural implication is significant: Anthropic, OpenAI, and Google have every incentive to commoditize the autonomous coding layer as fast as possible, because doing so forces enterprise buyers back to the API tier where the model providers capture the margin.

| Company / Product | Valuation (as of mid-2026) | Reported ARR | Product Architecture | Primary Buyer |

|---|---|---|---|---|

| Cognition (Devin) | $26B post-money (May 2026) | $492M (May 2026) | Autonomous agent — plans, writes, debugs, deploys; no human in loop | Enterprise IT / engineering leadership |

| Cursor | $29.3B (Nov 2025); ~$50B sought (early 2026) | Not publicly disclosed | IDE-integrated copilot — developer controls decision loop | Individual developers / dev teams |

| Anthropic (Claude Code) | Not separately valued (bundled in Anthropic) | Bundled in API and Pro/Team subscriptions | Autonomous coding agent via API + Claude.ai interface | Developers and enterprises via API tier |

| OpenAI (Codex) | Not separately valued (bundled in OpenAI) | Bundled in ChatGPT / API pricing | Autonomous coding agent via API + ChatGPT interface | Developers and enterprises via API tier |

| Google (Jules) | Not separately valued (part of Alphabet) | Bundled in Gemini / Google Cloud | Autonomous coding agent in Google IDE and Gemini ecosystem | Google Cloud enterprise customers |

Goldman, NASA, Mercedes: 50% Monthly Growth, Six Consecutive Months

Cognition's named enterprise customer list spans multiple regulated sectors: Tier-1 finance (Goldman Sachs, Santander, Citi, Itaú), U.S. government agencies (NASA, U.S. Army, U.S. Navy), automotive (Mercedes-Benz), technology services (Infosys, Cognizant), and hardware (Dell) . Enterprise usage grew more than 10× in 2026 alone, with 50% month-over-month expansion reported for six consecutive months heading into the Series D. This breadth — from Latin America's largest bank to U.S. military agencies to an automotive OEM — is unusual for a company under three years old and signals that enterprise procurement is taking autonomous coding seriously as a budget line item, not as a developer experiment.

"Devin completed a legacy system modernization in 8 days versus an estimated 8 months" — Mercedes-Benz case study cited in Cognition company materials, representing a reported 30× cycle-time reduction (source: TechFundingNews).

The government customer list raises compliance and security questions that most autonomous coding tools have not yet had to answer at scale. Whether Devin is running on air-gapped or FedRAMP-authorized infrastructure for military clients, how source code generated by the agent is handled under federal data handling requirements, and what the contract renewal structure looks like — none of this is disclosed publicly . Government contracts can be large but they operate on procurement cycles and security review processes that create lumpy, non-recurring revenue patterns. The customer logos are credibility signals; the contract structure is what determines revenue durability.

The Mercedes-Benz figure — 8 days versus 8 months — is the kind of case study that circulates widely in enterprise sales cycles, and it is credible as a directional data point for what autonomous agents can do on bounded, well-specified legacy modernization tasks. The relevant caveat is methodological: the "8 months" baseline is company-cited and the specification methodology for that estimate is not public. Read it as evidence of capability range, not as a precise operational benchmark that will reproduce identically across other customers or task types.

The $1B Investor Thesis: Autonomous Coding as Its Own Category

The core bet behind this round is that an autonomous software development layer can sustain independent commercial value separate from the foundation model providers — Anthropic, OpenAI, and Google — who are simultaneously Cognition's upstream suppliers and downstream competitors . Cognition's technology stack is a product and systems layer, not a pure model company: it combines proprietary models with API calls to OpenAI and Anthropic. This makes the company relatively asset-light on compute capex but structurally exposed to pricing changes or capability leapfrogs from those same providers.

"Autonomous agent infrastructure for software development can sustain independent valuations distinct from the underlying model providers" — investor thesis as described in The AI Insider's coverage of the Series D rationale.

Nine returning investors re-upped for the Series D alongside seven new names . In rounds at this scale, re-ups from existing backers are a meaningful signal: they had access to internal metrics the public does not and chose to increase their position. Broad coalition formation across venture risk profiles — Lux (deep tech), General Catalyst (platform), 8VC (enterprise), Ribbit (fintech), Founders Fund (long-duration bets) — suggests conviction is not concentrated in a single thesis camp. Multiple investor archetypes converging on the same round at $26B generally reflects that the internal data is compelling enough to override divergent priors.

The countervailing structural pressure is significant. Anthropic ships Claude Code updates on a fast cadence. OpenAI's Codex is actively developed. Google has Jules plus Google Cloud's enterprise distribution network and existing security certifications. Each provider has an incentive to narrow the gap on end-to-end task autonomy because doing so captures margin at the API layer. Cognition's defensibility argument is product surface area — integrations, workflow tooling, security compliance at the enterprise tier, and the switching cost of embedding an autonomous agent into a team's actual engineering process. That is a plausible moat at current revenue levels. Whether it holds at $1B ARR and beyond, when model providers may be operating at comparable autonomy levels, is what the next 24 months will test.

What the $26B Round Leaves Unresolved

Four questions remain open after the Series D. None of them preclude Cognition from being a large, successful company — but each is a variable that investors are pricing implicitly and external observers cannot price explicitly because the underlying data has not been disclosed.

- Margin profile. At 53× ARR, the valuation prices near-perfect execution. Gross margin and burn rate at $492M ARR have not been disclosed . An autonomous coding agent that makes API calls to OpenAI and Anthropic per task completion may have structurally lower gross margins than a typical SaaS business. The cost-per-task structure at enterprise scale is a critical variable for long-run valuation, and it is currently opaque.

- Windsurf ARR attribution. Organic Devin growth cannot be cleanly verified without a public revenue split. The 13× headline growth number is partially opaque as a result. This matters for forecasting whether the growth rate is product-led and self-sustaining or whether it will decelerate once Windsurf ARR contributions normalize.

- Growth durability. Sustaining 50% month-over-month expansion becomes arithmetically harder as the base approaches and exceeds $500M ARR. At $492M, reaching $1B by December requires adding roughly $508M in net new ARR across seven months — a larger absolute increment than the entire base twelve months ago. Churn, deal cycle length, and enterprise renewal rates are the operational variables that determine whether that rate can hold.

- Capital allocation. Use of the $1 billion raise has not been specified . Hiring pace, proprietary model development spend to reduce upstream API dependency, international enterprise expansion (implied by Mercedes-Benz adoption), and potential M&A are all open variables. Each allocation decision affects both the growth trajectory and the burn rate, and neither has been disclosed.

The 53× multiple is a bet that Cognition reaches $1B ARR by December 2026 and sustains enough growth beyond that point to justify the valuation at a more normalized exit multiple. At $492M in May with seven months remaining, the path is arithmetically plausible. Whether it is operationally achievable depends on variables that are, as of June 2026, either undisclosed or still unknown.

Frequently Asked Questions

What is Cognition AI's current ARR and how fast is it growing?

Cognition's ARR reached $492 million in May 2026, up from $37 million in May 2025 — 13× growth in twelve months . The company's stated target is to cross $1 billion in ARR before the end of 2026. Enterprise usage reportedly grew at 50% month-over-month for six consecutive months heading into the May 2026 Series D. One material caveat: part of the ARR growth includes revenue absorbed from the Windsurf asset acquisition in July 2025; Cognition has not publicly broken out the organic Devin-only contribution, which means the 13× headline cannot be fully verified as product-led.

How does Cognition's $26B valuation compare to Cursor and other rivals?

Cursor closed a $2.3 billion Series D at a $29.3 billion post-money valuation in November 2025 and was reportedly pursuing an additional $2 billion at a $50 billion valuation as of early 2026 . Cognition at $26B sits slightly below Cursor's November 2025 mark. Both companies operate in autonomous coding but differ architecturally: Devin owns tasks end-to-end with no human in the loop; Cursor augments a developer inside an IDE at the keystroke level. The model providers — Anthropic, OpenAI, Google — are not separately valued on their coding tools; those products are bundled into API and subscription pricing, making direct valuation comparisons with Cognition or Cursor structurally difficult.

What did Cognition gain from acquiring Windsurf's assets?

Cognition acquired Windsurf's SWE-1.6 model, hundreds of thousands of daily active users, and existing enterprise customer contracts in July 2025 . Google had separately acquired Windsurf's engineering team for approximately $2.4 billion earlier that year. The Cognition transaction captured product assets and an existing revenue base without the engineering talent — a product-and-ARR acquisition rather than an acqui-hire. The Windsurf ARR contribution has not been publicly broken out from Cognition's reported figures, which creates ambiguity in interpreting the 13× year-over-year growth headline as a measure of organic product-market fit.

Is a 53× revenue multiple justified for an AI coding startup?

Aggressive, but not unprecedented for a company reporting 13× year-over-year growth at this stage. High-growth AI application companies have cleared comparable multiples when revenue velocity is the primary underwriting variable. The key risks are: (1) margin profile — undisclosed, and potentially compressed by per-task API costs to OpenAI and Anthropic; (2) Windsurf ARR attribution — the organic-only growth rate is opaque; and (3) competitive pressure from Anthropic, OpenAI, and Google building comparable autonomous coding capabilities into their own products. The 53× multiple prices in sustained hypergrowth through the end of 2026 and into 2027. Whether that growth materializes at the required velocity is the central unresolved question for external analysis.

How does Devin differ from GitHub Copilot or Cursor?

Devin is designed as a fully autonomous software engineer: given a task description, it plans, writes, debugs, and deploys code without requiring a human decision at each step . GitHub Copilot and Cursor are IDE-integrated assistants — the developer controls the loop, approves or rejects suggestions, and makes every commit decision. The architectural difference drives distinct pricing models: outcome-based or task-based pricing for Devin versus per-seat subscriptions for copilot tools. It also drives different buyer profiles: enterprise IT or engineering leadership purchasing Devin at contract scale versus individual developers subscribing to Cursor or Copilot directly.

Where This Leaves Cognition — and the Autonomous Coding Market

The $26 billion Series D is not proof of product success — it is a priced bet on a specific future trajectory. At $492M ARR and 13× year-over-year growth, Cognition has built a scaled revenue base faster than almost any developer tools company on record. The customer list spanning Goldman Sachs, NASA, Mercedes-Benz, and the U.S. Army signals that enterprise procurement has moved past the pilot stage and is treating autonomous coding as a contractable line item. That is the strongest version of the bull case, and it is backed by real, named customers and a clear ARR trajectory.

The structural risk is the upstream dependency. Cognition is building on top of models from the same providers shipping competing products. Defensibility has to come from product surface area — enterprise integrations, workflow tooling, security compliance built to government standards, and the switching cost of embedding Devin into an organization's actual engineering process — rather than from model capability alone. That is a viable moat at current revenue levels; whether it sustains at $1B ARR and beyond depends on how fast Anthropic's Claude Code, OpenAI's Codex, and Google's Jules close the autonomy gap while adding their own enterprise distribution muscle.

For developers and technical founders assessing this market: the more immediately actionable question is not whether $26 billion is the right number, but whether autonomous coding agents are now mature enough to own a real slice of your engineering workflow. The Mercedes-Benz case study, the enterprise contract breadth, and the ARR trajectory suggest that question has already been answered affirmatively at the large enterprise tier. The individual developer adoption curve — and which product wins at that layer — is the next frontier worth watching.

Last updated: 2026-06-01. Based on publicly available information from the Series D announcement on May 27, 2026 and prior funding disclosures. Financial figures are as reported by Cognition and cited press coverage; audited financials have not been published.