How AI Token Futures Would Work

An AI token is the atomic billing unit for large language model consumption — roughly 0.75 English words per token, with both input prompts and output completions metered separately. Every major commercial LLM API globally — OpenAI, Anthropic, Google, Baidu, DeepSeek — uses tokens as the primary pricing basis. An AI token futures contract would let an enterprise lock in a forward price for that consumption, hedging against cost spikes the same way airlines use jet fuel futures to stabilize operating budgets. The proposed instrument prices the service-layer output — what a buyer pays per token consumed — not the underlying GPU compute rental that makes inference possible. That distinction is structurally important and separates it from what US exchanges are building simultaneously.

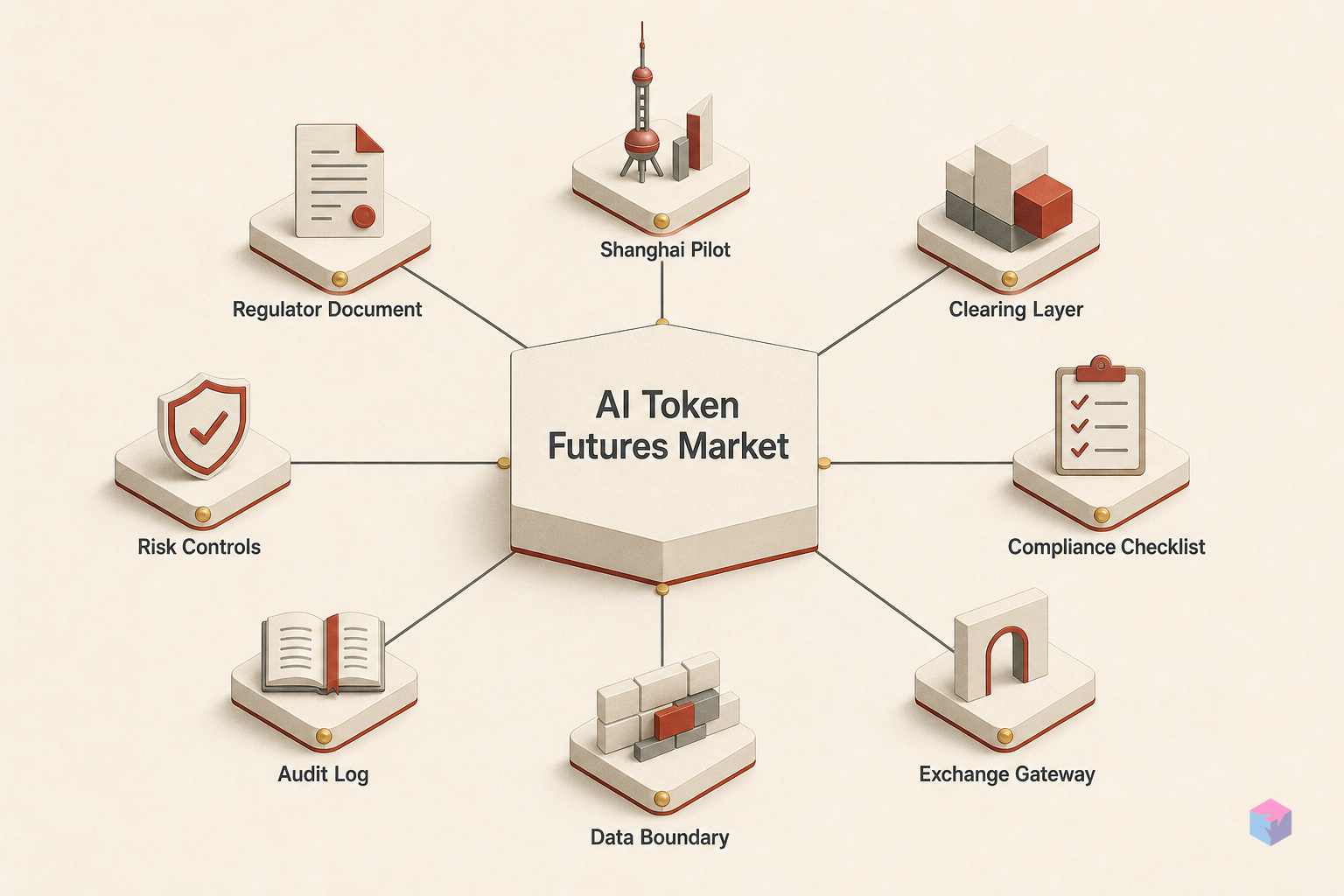

Quick Answer: Shanghai Futures Exchange (SHFE) is in early-stage research to design cash-settled futures contracts tied to AI token consumption — the standard per-unit billing for LLM API calls. Chinese government data shows daily token usage reached 140 trillion by March 2026 . No contract specs or regulatory filings exist yet; Baocheng Futures estimates a 3–5 year realistic launch horizon.

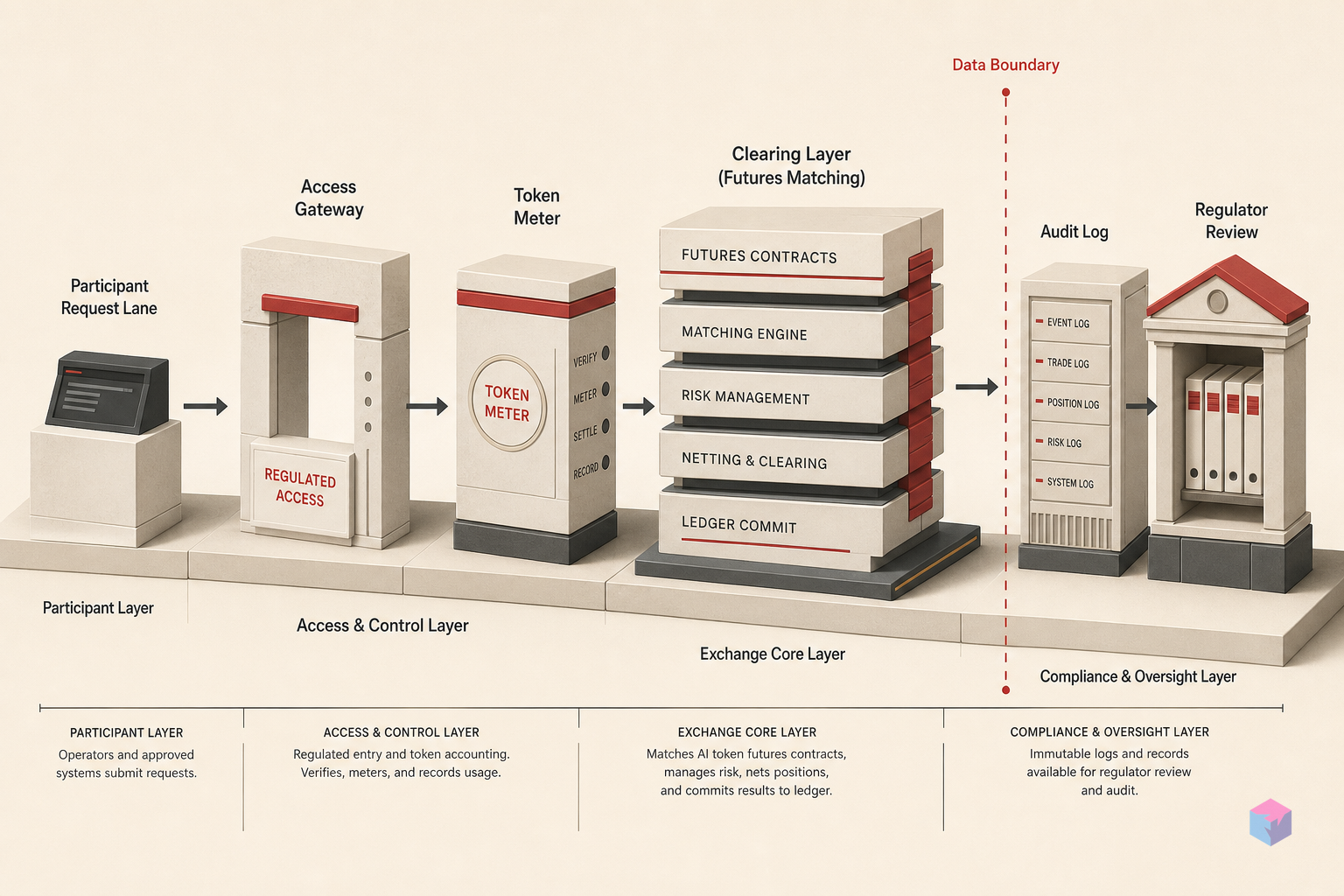

The settlement mechanics would follow the standard structure for cash-settled commodity futures. At expiry, contracts settle in cash against a benchmark index that tracks the prevailing market price for a standard token bundle across participating AI providers — no physical delivery of tokens occurs. This is where the core design problem lives: the index must be credible, tamper-resistant, and broadly accepted by market participants. Without a functioning benchmark, there is no contract. The index problem is the first-order unsolved challenge, and it is what separates this initiative from a functioning product.

The economic logic for the instrument is clean. AI token consumption is an operating cost for enterprises running production AI workloads. Token prices are set unilaterally by API providers and subject to market pressures — they can move in response to compute supply constraints, competitive dynamics, and demand surges. A company spending several hundred thousand dollars monthly on AI inference cannot easily absorb mid-cycle price swings of 20–30%. A forward price lock converts that uncertain cost into a planned fixed cost, which is the standard corporate rationale for commodity hedging.

Settlement reference design aside, token futures address something GPU compute futures do not: the consumption layer. Even if an enterprise has no GPU exposure — it buys API access from a provider and has no involvement in infrastructure — it still carries token price risk. According to Reuters via Yahoo Finance, SHFE's initiative explicitly targets this service-layer exposure, positioning it as a structurally distinct product rather than a duplicate of what CME and ICE are developing.

China's AI Consumption Numbers That Justify the Instrument

Official Chinese government data shows daily AI token consumption in China grew 1,000-fold from early 2024 to more than 140 trillion tokens per day by the end of March 2026 . That trajectory — implying a baseline of roughly 140 billion tokens per day in early 2024 — is the demand signal SHFE is treating as economic justification for a financial instrument. At 140 trillion tokens consumed daily, a 10% forward price swing represents substantial enterprise budget exposure across the Chinese economy. The hedging use case is not theoretical; it follows directly from the scale of consumption.

| Period | Estimated Daily AI Token Consumption (China) | Key Context |

|---|---|---|

| Early 2024 | ~140 billion tokens/day (implied baseline) | Early enterprise LLM adoption; limited consumer AI app penetration |

| Mid-2024 to 2025 | Rapid acceleration (no official interim figures published) | DeepSeek model releases; scaling enterprise API integrations; consumer app growth |

| End of March 2026 | >140 trillion tokens/day | Consumer AI apps at scale; agentic pipelines; enterprise automation workloads |

The growth in consumption has outpaced available compute supply. Several Chinese AI model providers have moved to ration user access due to compute shortages, according to Reuters reporting. Rationing is a leading indicator of price volatility: when supply is constrained against exponentially growing demand, token prices can move sharply and unpredictably. That is the precise risk profile that a futures market is designed to address.

For Chinese enterprises running AI-intensive workloads — e-commerce platforms using LLM-based recommendations, financial institutions using AI for document processing, software companies with production agent infrastructure — monthly API spend has become a material operating cost line. The 1,000x consumption growth figure makes this a quantitatively concrete problem, not a forward-looking concern. According to The Standard's coverage, the rationing behavior already observed at Chinese AI providers is a direct symptom of the supply-demand imbalance the futures instrument would help manage.

The same consumption numbers create exposure on the provider side. Chinese AI model operators price tokens competitively while managing GPU compute input costs. When hardware costs increase — as the Ornn Blackwell GPU index data demonstrates can happen sharply — providers face margin compression unless they raise token prices, which competitive pressure may prevent. A token futures market gives providers a revenue-side hedge that is independent of their compute cost exposure.

Token Futures vs. GPU Compute Futures: Two Different Instruments

GPU compute futures and AI token futures target different nodes in the AI supply chain. GPU compute futures — announced by CME Group and under development at ICE in the United States — price the cost of renting GPU hardware by the hour. That is the infrastructure input: the raw compute capacity that model providers purchase to run inference. SHFE's proposed AI token futures would price the model output consumption: the per-token cost that an enterprise buyer pays when calling an AI API. The two instruments are complementary, not redundant. A vertically integrated company — running its own inference infrastructure while also buying API capacity from other providers — could hold positions in both independently, hedging across the full cost structure of its AI operations.

| Attribute | GPU Compute Futures | AI Token Futures |

|---|---|---|

| What is priced | GPU rental cost per GPU-hour | AI model output cost per token |

| Supply chain node | Infrastructure / input layer | Service / consumption layer |

| Exchange | CME Group, ICE (United States) | SHFE (China — proposed) |

| Index provider | Silicon Data (CME), Ornn (ICE) | Not yet defined — core unresolved obstacle |

| Primary hedger | AI model providers, data centers, GPU cloud buyers | Enterprise API consumers, model operators |

| Settlement method | Cash-settled against benchmark index | Cash-settled (proposed) — benchmark methodology TBD |

| Development status (May 2026) | Announced; pending regulatory review | Early-stage SHFE feasibility research; no specs filed |

Ornn's index data provides a concrete illustration of why infrastructure hedging demand is real: Nvidia Blackwell GPU spot rental prices surged 48% between mid-February and mid-April 2026, moving from $2.75 to $4.08 per GPU-hour . For a model provider running inference on Blackwell hardware, that 48% increase in a 60-day window is a direct cost shock. That same shock propagates — with a delay and at variable rates — into the token prices that API consumers face, depending on provider competitive positioning and contract structures.

The correlation between GPU compute cost and token price is real but imperfect. Providers absorb or pass through hardware cost changes at different rates depending on capacity utilization, competitive dynamics, and existing customer contracts. This imperfect correlation is precisely the condition under which both instruments are independently useful. A model provider could use GPU compute futures to hedge its input costs while offering token buyers a stable forward price — and token buyers could hedge against residual consumption price volatility through token futures independently of the provider's hedging position.

For a developer or technical founder: if your application runs a material volume of tokens through a Chinese AI API, your cost exposure is entirely on the service layer. GPU compute futures being developed in the US offer you no direct hedge because you are not renting GPUs — you are consuming model output. That is the market gap SHFE is positioning to fill, and why the two products are structurally complementary rather than competitive.

CME and ICE: What US Exchanges Already Have in Motion

On May 12, 2026, CME Group and Silicon Data jointly announced plans to launch the world's first GPU compute futures, pending regulatory review and targeting a launch later in 2026 . The contracts would be indexed to Silicon Data's daily GPU rental rate benchmarks and cash-settled against that index at expiry. According to Markets Media, the partnership applies CME's established derivatives infrastructure to Silicon Data's transaction-based GPU rental benchmarks — the same model that has worked for energy and metals commodity futures.

"Today's announcement marks the first time compute capacity has a standardized, exchange-traded futures market — giving enterprises a tool to manage the GPU cost volatility that has made AI infrastructure budgeting unpredictable," — CME Group and Silicon Data, joint announcement via PR Newswire, May 12, 2026

Sixteen days after the CME/Silicon Data announcement, Reuters published its exclusive on SHFE's token futures research. The Reuters report explicitly frames China's initiative as a strategic response to US exchange momentum. The geopolitical dimension is direct: the exchange that builds dominant price discovery infrastructure for AI compute shapes how AI services are valued and risk-managed globally. Setting the benchmark methodology — like Brent and WTI in crude oil — is a form of standards influence that extends beyond any single market.

Intercontinental Exchange — parent company of the NYSE — is developing a parallel GPU compute futures product in partnership with Ornn, an index provider tracking GPU spot rental markets. According to The Next Web, the ICE product would be cash-settled against Ornn's Blackwell GPU spot rate data. The 48% price surge from $2.75 to $4.08 per GPU-hour that Ornn's index captured between February and April 2026 provides the volatility evidence that makes the hedging product commercially compelling to potential users.

Both US products target the compute rental market — GPU hours, not token consumption. This leaves a structurally distinct product niche open for China's proposed token futures, if it can solve the index standardization problem. The US exchanges are building hedging infrastructure for the infrastructure layer; China is proposing hedging infrastructure for the usage layer. Whether the two approaches eventually converge into a unified global AI cost hedging market depends on whether token prices and GPU rental rates become sufficiently correlated and transparent to underlie a single instrument — a question that market development over the next several years will answer.

Who Bears the Cost Exposure: Enterprise Buyers and Providers

A liquid futures market requires both buyers and sellers of forward price risk. The viability of SHFE's eventual product depends on whether enough participants with genuine opposing exposures materialize — the same condition that made energy futures markets work. Four participant groups represent the potential constituency for AI token futures, each with a different risk profile that the instrument would address.

Large enterprise API consumers are the clearest use case. Organizations running production AI workloads at scale — where monthly token consumption is a significant operating budget item — face uncertainty when token prices move mid-budget-cycle. A company that cannot absorb 20–30% price swings without replanning needs a forward price lock mechanism. This group maps to the enterprise customer base of major Chinese AI API providers: large technology companies, financial institutions, logistics operators, and consumer internet platforms that have embedded LLM functionality into their core products. These are the entities that would be natural buyers of token futures to hedge consumption costs.

Chinese AI model providers hold the natural opposite position. Their revenue is denominated in token prices; their costs are primarily in GPU compute and operations. When hardware costs rise faster than token prices (which competition may prevent providers from raising), providers absorb margin compression. Token futures give providers a revenue-side hedging mechanism — locking in forward revenue on expected token delivery — independent of their compute cost exposure. This supply-side participation is essential for liquidity; a token futures market where only buyers are hedging consumption risk is structurally one-sided.

Data center operators represent a third stakeholder category with a different motivation. Investment cycles for AI inference infrastructure run 12–36 months. A liquid futures market for AI token demand would provide forward pricing signals that data center operators could use to calibrate capacity expansion decisions: if forward token prices are elevated relative to current infrastructure build costs, the market is signaling forward demand justification for additional capacity. This price discovery function — aggregating dispersed forward-looking demand information into a public price signal — is one of the less-discussed but genuinely valuable functions of commodity futures markets.

Financial institutions would build the structured products layer and provide market-making liquidity. Chinese commodity trading desks at major brokerages already operate in energy, metals, and agricultural futures. Extending that operational infrastructure to AI token futures is tractable once the underlying exchange contract exists. These institutions also serve as intermediaries for corporate hedgers that cannot manage continuous exchange positions: a mid-sized enterprise could buy an over-the-counter structured product from a bank's trading desk, with the bank hedging its own book through the exchange.

Fragmentation: The Core Structural Obstacle

The most significant barrier to launching AI token futures in China is not regulatory appetite or exchange readiness — it is the absence of a standardized token price benchmark. Every Chinese AI provider prices tokens on its own scale: different models carry different per-token prices, context window length affects effective token costs, and pricing structures vary across providers. Without a standardized reference index, there is no contractual underlying to settle against. The equivalent in energy markets would be attempting to design crude oil futures without a Brent or WTI benchmark. The number to cash-settle against does not exist, and until it does, no contract can be written.

"Market fragmentation is the primary structural barrier to a near-term launch — AI service providers each operate their own token pricing frameworks, and without a credible, standardized industry benchmark, no exchange-traded contract can be designed around a stable and auditable reference rate," — Research Note, Baocheng Futures, May 2026

The fragmentation problem runs deeper than naming conventions or unit definitions. Token costs are not homogeneous even within a single provider's API. A token in a short-context completion has different KV-cache and memory utilization characteristics than a token in a 128K-context completion. Reasoning-intensive models cost more per token to serve than retrieval-focused models with the same parameter count. Batch inference pricing differs from real-time inference pricing. A benchmark index must define a standard basket of token consumption that is economically meaningful to hedgers and technically auditable by regulators — a non-trivial methodology problem that has no obvious settled answer.

The most plausible resolution paths mirror how the US GPU compute market addressed the same problem. In the US, third-party index providers — Silicon Data for CME, Ornn for ICE — built proprietary transaction-based benchmarks from actual market data. In China, two parallel paths exist: the CSRC could mandate an industry-standard token pricing framework using regulatory authority to compel standardization, or a third-party index provider could emerge to build a voluntary transaction-based benchmark. The regulatory mandate path is faster in principle but involves significant industry negotiation; the voluntary index path requires a sufficient number of AI providers to contribute pricing data and accept a shared methodology — which creates competitive sensitivity.

No third-party Chinese token price index provider currently exists in this space, based on public reporting. Building one requires aggregating real transaction data from AI providers, designing a methodology that survives legal and commercial challenges, and establishing enough market credibility that exchange participants will accept it as a settlement reference. This is multi-year work under favorable conditions. According to Crypto Briefing's coverage of the SHFE initiative, the index creation problem is recognized as the longest-lead-time item in the full development sequence — which is a significant contributor to Baocheng Futures' 3–5 year horizon estimate.

Regulatory Gatekeeping and the 3–5 Year Horizon

The China Securities Regulatory Commission (CSRC) is the approval authority for any new exchange-traded derivatives product in China. As of May 2026, the CSRC declined to comment on Reuters' reporting about SHFE's research initiative . No contract specifications have been drafted, no regulatory application has been filed, and the core prerequisite — a standardized token price benchmark — does not exist. SHFE is conducting early-stage feasibility research. The distance between "early-stage research" and "live contract" is measured in years and involves multiple sequential dependencies, each with execution risk.

Baocheng Futures' May 2026 research note estimated a realistic launch horizon of 3–5 years. That is a brokerage estimate, not an official government commitment or a statement by SHFE or the CSRC. It reflects the realistic sequencing of what must be completed before trading can begin. The full prerequisite chain looks like this:

- Token benchmark standardization — An industry-accepted methodology and index for Chinese AI token prices. This is the prerequisite for all subsequent steps and has the most unresolved technical questions. No existing institution has been mandated or has volunteered to build it.

- SHFE contract design — Contract specifications including lot size, tick size, expiry schedule, margin requirements, and settlement procedure. Standard derivatives engineering applied to a novel underlying asset class — tractable once the benchmark exists.

- CSRC filing and regulatory review — The CSRC's review process for new derivatives products typically runs 12–24 months from a complete filing. The commission must be satisfied that the product serves legitimate hedging purposes, does not create systemic risk, and operates within the existing regulatory framework for commodities and financial derivatives.

- Market maker recruitment — Exchange-traded futures require committed market makers providing continuous two-sided liquidity. Financial institutions must be willing to take on the inventory risk of making markets in a novel instrument with limited initial trading volume.

- Liquidity bootstrapping — Initial trading volumes are thin for any new futures product; the exchange and participants must manage through a ramp-up period before the contract becomes economically useful for corporate hedgers who need tight bid-ask spreads and depth.

The CSRC's silence on the Reuters report leaves regulatory appetite genuinely unknown. China has a track record of both moving quickly on financial product innovation when it serves strategic goals and moving cautiously when products raise systemic risk concerns. AI token futures sit at that intersection. The strategic goal — building Chinese financial infrastructure for the AI economy ahead of US exchange dominance — is apparent from the Reuters framing. The systemic risk question — whether a liquid speculative market in AI token prices could amplify volatility or create manipulation risks — is the kind of concern that extends regulatory review timelines.

Frequently Asked Questions

What exactly is an AI token in the context of these futures contracts?

An AI token is the atomic unit of measurement for large language model computation — approximately 0.75 English words per token, though the exact ratio varies by tokenizer and language. When you call a commercial LLM API, both your input prompt and the model's output response are counted and billed in tokens. Every major commercial AI API globally — OpenAI, Anthropic, Google, Baidu, DeepSeek, and others — uses tokens as the primary billing unit. One million tokens corresponds to roughly 750,000 words of text. For the proposed futures contract, the token is the underlying commodity unit: the contract would let buyers and sellers agree today on the forward price for a specified quantity of tokens to be consumed in a future period, enabling enterprises to lock in AI service costs ahead of actual consumption.

How are AI token futures structurally different from GPU compute futures?

GPU compute futures, being developed at CME Group and ICE in the United States, track the cost of renting GPU hardware by the hour — the infrastructure input that AI model providers buy to run inference. If you are a model provider purchasing GPU capacity from a cloud vendor, GPU compute futures hedge your input cost exposure. AI token futures, as proposed by SHFE, would track the cost of consuming AI model outputs at the API level — what an enterprise pays per token when calling an AI service. These are different supply chain nodes: one is the raw compute cost paid by infrastructure buyers and model providers; the other is the model output cost paid by API consumers. A company that runs its own inference infrastructure and sells API access could hold positions in both instruments simultaneously, hedging its hardware input costs with GPU compute futures and its service revenue volatility with token futures. The two instruments address different exposures and can coexist without redundancy.

What is the main technical problem preventing these contracts from launching now?

Market fragmentation — Chinese AI service providers each use their own token pricing framework, with no standardized reference methodology across the market. A futures contract must cash-settle against a credible, agreed-upon reference index at expiry. Without a benchmark equivalent to Brent crude for oil futures or Ornn's Blackwell rate for GPU futures, there is no number to settle against and no valid contract can be structured. According to Baocheng Futures' May 2026 research note, this fragmentation is the primary structural barrier to near-term launch. The problem is compounded by heterogeneity within individual providers: reasoning models, retrieval models, short-context and long-context completions, and batch versus real-time requests all have different cost profiles even for the same raw token count — any benchmark methodology must handle that heterogeneity in an auditable, agreed-upon way before the contract can be defined.

Can international developers or enterprises access SHFE-listed AI token futures?

No contract exists yet. Beyond that, SHFE operates primarily as a domestic Chinese exchange, and foreign access to Chinese commodity futures markets is generally restricted under current regulations. Even for commodity futures SHFE currently lists, foreign participant access requires specific regulatory approvals and is not generally available to international retail or smaller institutional participants. If AI token futures eventually launch, cross-border access for international developers or enterprises is unlikely at launch. International participants looking to hedge AI service cost exposure in the nearer term should monitor CME Group and ICE's GPU compute futures products, which are under US regulatory frameworks with more established pathways for foreign participant access — though those instruments address hardware cost exposure, not API consumption cost.

When could AI token futures realistically launch in China?

Baocheng Futures' May 2026 research note estimates 3–5 years as the realistic horizon. As of May 2026, SHFE is conducting early-stage feasibility research with no contract specifications drafted and no regulatory filing made with the CSRC. The CSRC itself declined to comment on Reuters' reporting. The full prerequisite sequence — constructing a standardized token price index, designing contract specifications against that index, filing with the CSRC and completing regulatory review, recruiting market makers, and bootstrapping liquidity — has not yet begun in earnest at any stage. The 3–5 year estimate assumes this sequence proceeds without major regulatory or technical setbacks, which is an optimistic baseline given that the index — the first and longest-lead-time prerequisite — has no clear development roadmap or institution assigned to build it as of May 2026.

Two Exchanges, Two Supply Chain Nodes, One Race

The parallel US and Chinese exchange developments in May 2026 represent a concrete step toward treating AI compute as a financial commodity — two different supply chain nodes being financialized at roughly the same time. CME and ICE are pricing the infrastructure input (GPU hours); SHFE is researching how to price the service output (token consumption). If both succeed, enterprises will eventually be able to hedge their AI cost exposure at multiple points in the value chain, the way sophisticated energy consumers hedge both crude feedstock and refined product costs independently.

The nearer-term actionable signal is on the US side. CME Group and Silicon Data's GPU compute futures are further along the development curve — announced with pending regulatory review, not early-stage research. If you manage GPU infrastructure purchasing or cloud compute budgets, those instruments will be worth tracking as they move toward live trading. The SHFE token futures initiative is a planning-horizon item: relevant to enterprise AI budget strategy over a 3–5 year window, not a near-term operational consideration.

The index standardization problem is the specific technical thread worth following for the token futures story. A credible Chinese AI token price benchmark — whether mandated by the CSRC or built by a third-party index provider — would be useful independent of whether SHFE's futures product ever launches. Even as a reference rate for bilateral enterprise contracts and budget planning, a standardized token price index improves market transparency. Watch for CSRC consultation papers or Chinese AI industry working groups on token pricing methodology; those are the leading indicators that the foundational infrastructure is being built, and they will precede any exchange product by at least a year.

Last updated: 2026-05-30. Based on Reuters exclusive published May 28, 2026 , CME Group and Silicon Data joint announcement of May 12, 2026 , and Baocheng Futures research note issued May 2026.